Customs valuation methodology selection

When a nominationproduct arrives at the terminal and a parcel is registered in Atlas, the value of the parcelproduct is recorded by CS in line with the current market value.value at the time of registration. The market value is usually provided by the customer.customer, Otherwise,or it isotherwise obtained by CS from publicly available market data sources, such as Platts Market Data from S&P.

When the customer sends a nomination to bring the product into free circulation, CS registers an import service in ERP. The import service requires a value, which is used in the import declaration.

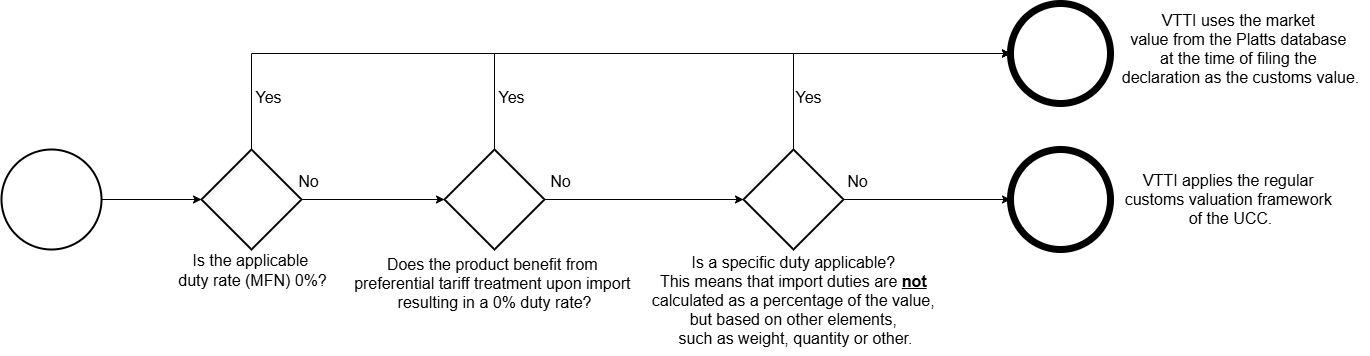

Where the applicable import duty rate is 0%, the goods qualify for preferential treatment upon import, or where a specific duty applies (i.e., duties are not calculated over the value but over another factor such as weight), the customs value declared serves a purely statistical purpose and has no financial impact. In such cases, VTTI has agreed with the customs authorities to apply the “reasonable means” method as an alternative method of customs valuation, in accordance with Article 74(3) of the UCC. More specifically, VTTIthe determinesmarket value that was registered at the time the parcel was created is used as the customs value onin the basisimport of the current market value of the relevant product.declaration.

If the import duty rate exceeds 0%, no preferential treatment applies and customs duties due are calculated on an ad valorem basis, the regular customs valuevaluation will in principle be determined in line with the transaction value method, in accordance with article 70framework of the UCC.UCC will be applied to determine the customs value.

This approach can be schematically displayed as follows: