Work instruction

In practice, there are two types of documents that refer to non-preferential origin:

An official Certificate of Origin (CoO), which exporters can obtain by applying to the competent Chamber of Commerce or the relevant customs authorities; and

A commercial document declaring the non-preferential origin (Terminal Origin Declaration).

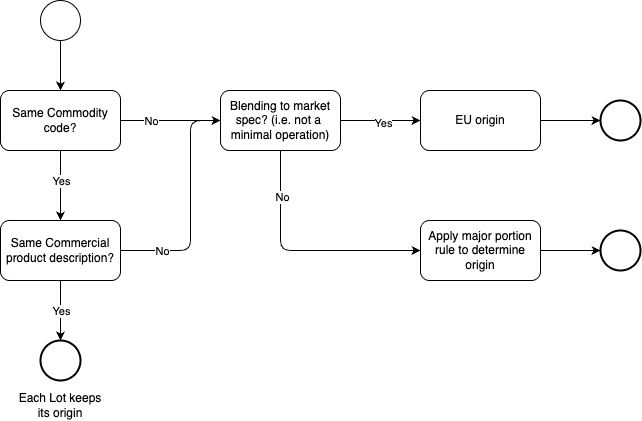

Upon request, our terminal can assist with the application for the relevant certificate or document via a broker authorised to apply for an official CoO (digital connection required). Regarding commercial documents, our Customer Service team determines the non-preferential origin in accordance with the following criteria:

Below some concrete examples on applying the procedure for establishing the non-preferential origin.

1. Products added to the “base” product may enhance or improve it, but do not alter its essential nature. Such activities are considered minimal operations and do not confer origin.

As this involves blending rather than mere storage, the major portion rule applies, provided that customers inform us of the origin and substantiate it with appropriate documentation. This requirement applies at least to the parcel representing the major portion based on weight. The origin of the remaining parcels may be unknown without affecting this assessment.

As this involves blending rather than mere storage, the major portion rule applies, provided that customers inform us of the origin and substantiate it with appropriate documentation. This requirement applies at least to the parcel representing the major portion based on weight. The origin of the remaining parcels may be unknown without affecting this assessment.

| Components | |||||

| Tank | Product | Commodity code | Status | Kilogram | Liters 15 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | 35.096.530 | 45.579.910 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | 244.894 | 349.849 |

| Blended product | |||||

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | 35.341.424 | 45.929.758 |

2. Various components blended into a specific product (which itself is also used as a component) may be regarded as deliberate and proportionate blending and therefore origin-conferring.

The processed product results from the combination of several significant components. The fact that one of these components shares the same Commodity code as the final product does not alter this assessment. In quantitative terms, it is not considered a “base” product to which only minimal operations are applied. Accordingly, a new product is deemed to have been created.

The processed product results from the combination of several significant components. The fact that one of these components shares the same Commodity code as the final product does not alter this assessment. In quantitative terms, it is not considered a “base” product to which only minimal operations are applied. Accordingly, a new product is deemed to have been created.

| Components | |||||

| Tank | Product | Commodity code | Status | Kilogram | Liters 15 |

| T x | Gasoline RON 91 | 2710 1241 90 | T1 - Bonded | 28.077.224 | 36.463.928 |

| T x | Naphta | 2710 1225 90 | T1 - Bonded | 5.565.992 | 7.951.417 |

| T x | Alkylate | 2710 1290 90 | T2 - Excise controlled | 4.634.938 | 6.019.400 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | 17.670.712 | 22.948.977 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | 244.894 | 349.849 |

| Blended product | |||||

| T x | Gasoline RON 95 | 2710 1245 90 | T1 - Bonded | 33.643.216 | 44.415.345 |

3. Various components (classified under the same Commodity code but possessing different technical characteristics) blended into a specific product may be regarded as deliberate and proportionate blending, thereby conferring origin, provided that the resulting product acquires new technical specifications or attributes that it did not possess prior to blending. The fact that all components share the same Commodity code as the final product is not relevant.

| Components | |||||

| Tank | Product | Commodity code | Status | Kilogram | Liters 15 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | 427.486 | 429.112 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | 4.634.938 | 4.617.392 |

| T x | IMFO | 2710196800 | T2 - Excise controlled | 5.565.992 | 5.587.141 |

| T x | Cutterstock | 2710196800 | T1 - Bonded | 43.870.663 | 44.037.332 |

| Blended product | |||||

| T x | HSFO | 2710196800 | T1 - Bonded | 54.743.046 | 54.915.871 |