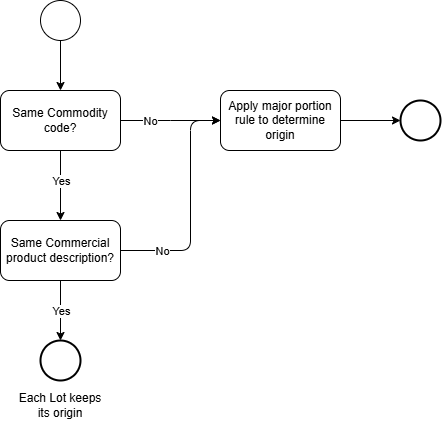

Work instruction (simplified process)

In practice, there are two types of documents that refer to non-preferential origin:

An official Certificate of Origin (CoO), which exporters can obtain by applying to the competent Chamber of Commerce or the relevant customs authorities; and

A commercial document declaring the non-preferential origin (Terminal Origin Declaration).

Upon request, our terminal can assist with the application for the relevant certificate or document via a broker authorised to apply for an official CoO (digital connection required). When applying with the Chamber of Commerce the burden of proof is greater than when issuing a Terminal Origin Declaration, because the latter is not an official document and it is the discretion of the Terminal to conclude on origin and the proof that is provided. For example, when documentation is provided that the Product comes from a refinery in Italy the Terminal may be inclined to accept this as sufficient proof, where the Chamber of Commerce is likely to require a Suppliers declaration for non-Preferential origin. Apart from whether or not the proof of origin for the components is sufficient or not, the procedure in determining the origin should be the same with the terminal itself and the Chamber.

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.096.530 | 45.579.910 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

| Blended product | ||||||

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.341.424 | 45.929.758 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | Gasoline RON 91 | 2710 1241 90 | T1 - Bonded | Norway | 28.077.224 | 36.463.928 |

| T x | Naphta | 2710 1225 90 | T1 - Bonded | Unknown | 5.565.992 | 7.951.417 |

| T x | Alkylate | 2710 1290 90 | T2 - Excise controlled | Unknown | 4.634.938 | 6.019.400 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Unknown | 17.670.712 | 22.948.977 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

| Blended product | ||||||

| T x | Gasoline RON 95 | 2710 1245 90 | T1 - Bonded | Unknown | 56.193.763 | 73.733.571 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | IMFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | Cutterstock | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 54.743.046 | 54.915.871 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |