Preferential origin - Specific EU - UK TCA Procedures

Here various procedures are listed describing the rules of origin as specified in the specific Preferential trade agreements between the exporting and importing countries, providing the basis for preferential tariff treatment.

- EU-UK TCA for Tariff Heading 2710 - Terminal operations

- Statement on origin

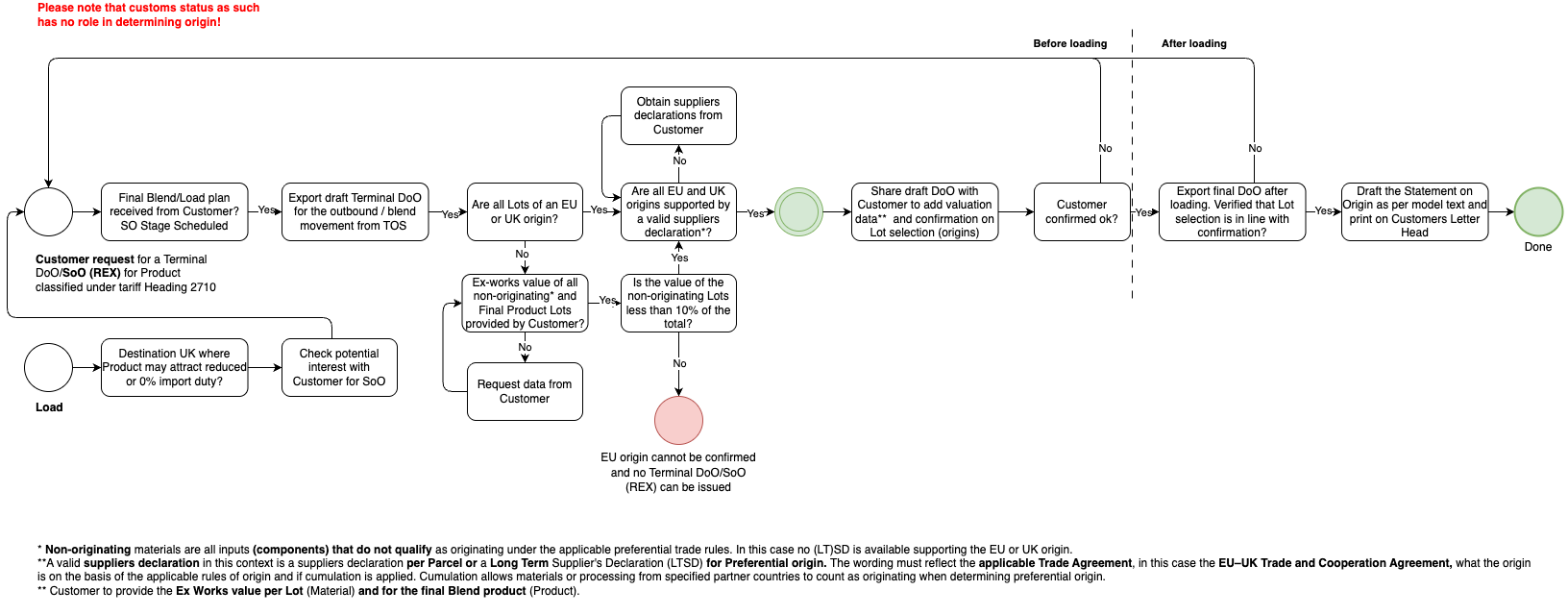

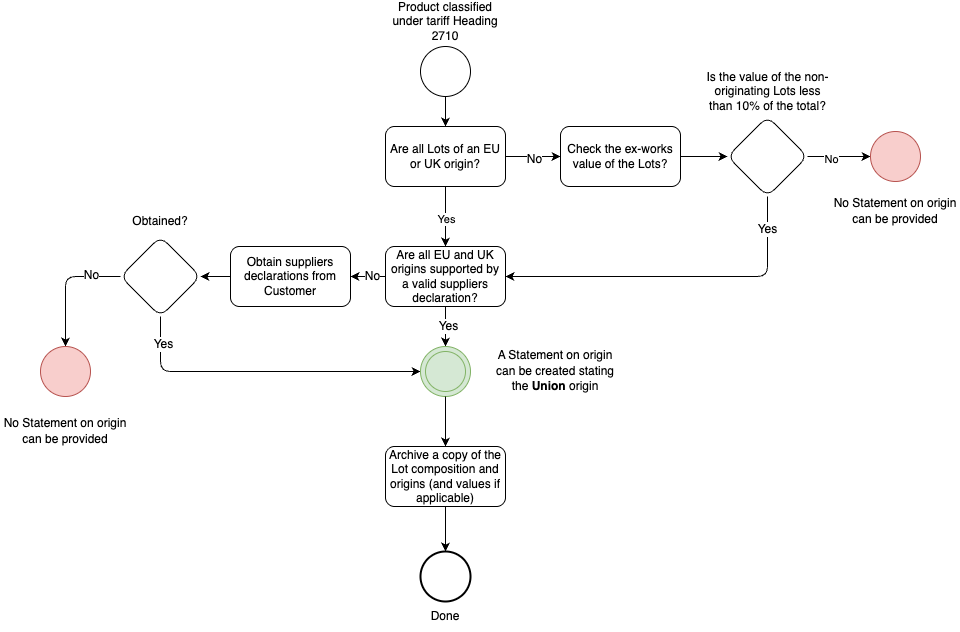

- SOP - Decision flow Preferential origin EU - UK TCA tariff Heading 2710

- Decision flow Preferential origin EU - UK TCA tariff Heading 2710

- Template preferential origin (long term) supplier declaration

EU-UK TCA for Tariff Heading 2710 - Terminal operations

1. Purpose and Scope

This procedure outlines how to determine and maintain preferential origin status for petroleum products classified under tariff heading 2710 that are stored, handled, or blended in the EU or the UK under the EU-UK Trade and Cooperation Agreement (TCA).

Tariff Heading 2710 covers:

Petroleum oils and oils obtained from bituminous minerals (other than crude); preparations not elsewhere specified or included, containing by weight 70% or more of petroleum oils or of oils obtained from bituminous minerals.

It applies to all facilities and operators engaged in:

Storage and distribution of petroleum products of EU or UK origin;

Occasional blending or addition of non-originating material (e.g. additives, stock adjustments);

Origin tracking using accounting segregation methods.

The aim is to ensure that stored goods maintain or correctly lose their preferential origin status in compliance with the TCA.

2. Legal Framework

EU-UK Trade and Cooperation Agreement (TCA): Title I, Rules of Origin (Part Two, Heading One, Chapter 2).

Annex ORIG-2: Product-Specific Rules (PSR) for HS 2710.

Article ORIG.14:Accounting segregation.

Article ORIG.12:Tolerances for non-originating materials.

Article ORIG.7:Insufficient working or processing operations.

3. Product-Specific Rule (PSR) - HS 2710

"Manufacture from materials of any heading, except that of the product, provided that the value of all non-originating materials used does not exceed 40% of the ex-works price of the product."

Non-originating materials under the same heading (2710) may not be used.

Materials classified under other headings (e.g. 2709 crude petroleum) may be used, provided the value of all non-originating inputs does not exceed 40% of the ex-works price.

The product must undergo a Change in Tariff Heading (CTH) as part of the transformation.

For storage and distribution activities, this PSR is relevant primarily for verifying that minor additions of non-originating material do not exceed permissible thresholds and that the overall product maintains its preferential origin.

4. Cumulation

The EU-UK TCA allows bilateral cumulation only.

Materials originating in the UK are treated as originating in the EU and vice versa.

Inputs from third countries cannot be cumulated.

5. Key Operational Principles

5.1 Storage Does Not Alter Origin

-

Merely storing, transferring, or handling originating goods does not affect their preferential origin status, provided:

-

The goods remain identifiable, and

-

No operations are performed that would constitute insufficient working or processing under Article ORIG.7.

-

5.2 Insufficient Operations

Origin is not maintained if operations performed are limited to:

-

Simple blending of oils;

-

Simple mixing, dilution, or packaging;

-

Any process that does not result in a change in tariff heading or essential character.

However, for companies managing mixed stocks of originating and non-originating petroleum products, accounting segregation (Article ORIG.14) may be applied to maintain compliance without physically separating each batch.

5.3 Sufficient Working or Processing

Processing that qualifies:

Refining crude petroleum (heading 2709) into petroleum products (heading 2710);

Chemical transformation changing the essential character of the product.

Processing that does not qualify (as per Article ORIG.7):

Simple mixing of products;

Simple dilution;

Simple packaging or relabelling;

Any process that does not alter the tariff classification or essential character.

5.3.1 Origin Verification Process Manufacturing

Classify the product under CN 2710.

List all inputs with tariff headings and origin status.

Calculate the ex-works price of the finished product.

Determine total value of non-originating inputs.

If ≤ 40% of ex-works price = condition satisfied.

Ensure that no non-originating material of heading 2710 is used.

Confirm that the transformation changes the tariff heading (CTH achieved).

If all criteria are met, the product acquires EU or UK originating status.

6. Accounting Segregation (Article ORIG.14 TCA)

6.1 Principle

Accounting segregation allows an operator to manage originating and non-originating materials or products in a single inventory where physical segregation is impractical.

This method may be used only if the records and control systems ensure that:

-

The quantities of originating and non-originating goods are accurately accounted for;

-

No more originating goods are deemed to be exported than those that would result from physical segregation.

6.2 Implementation Steps

-

Approval

-

Accounting segregation may be applied only if the operator has an approved origin accounting system validated by internal customs or compliance management.

-

-

Inventory System Requirements

-

The system must record:

-

Opening stock balance by origin category (EU, UK, non-originating);

-

Receipts (by origin and quantity);

-

Dispatches (with declared origin and supporting documentation).

-

-

The system must allow traceability from incoming to outgoing quantities.

-

-

Calculation Basis

-

The ratio of originating to non-originating goods in storage determines the share of outgoing goods that may be considered originating.

-

Example:

-

Stock: 90% originating + 10% non-originating.

-

A dispatch of 1,000 tonnes may be declared as originating up to 900 tonnes.

-

-

-

Documentation

-

Each origin batch movement must be supported by supplier declarations, statements on origin, or other valid proof.

-

Periodic stock reconciliation must confirm that cumulative declarations do not exceed available originating stock.

-

-

Retention

-

Records must be kept for a minimum of three years and made available upon customs request.

-

7. Incorporation of Non-Originating Material - 10% Value Tolerance

7.1 Legal Basis

Article ORIG.12 of the EU-UK TCA permits a tolerance of up to 10% of the ex-works price for non-originating materials used, even where the PSR would otherwise prohibit such use.

This tolerance cannot be used to exceed the maximum non-originating material limit (40%) specified in the PSR.

7.2 Application to HS 2710 (Storage Context)

In storage operations where non-originating material (e.g. additive or stabiliser) is added to otherwise originating petroleum products:

-

The value of the non-originating addition must not exceed 10% of the ex-works price of the final blended product.

-

The blended product may still be regarded as originating, provided:

-

The total non-originating material (including the addition) does not exceed 40% of the ex-works price; and

-

The blending does not fall within insufficient operations (i.e., must have a legitimate commercial purpose and not merely be a simple mix).

-

7.3 Calculation Example

-

Ex-works price of blended product: USD 1,000 per tonne

-

Non-originating additive: USD 80 per tonne (8%)

-

Total non-originating materials: 8% (<10%)

= Product retains preferential origin under the 10% tolerance rule.

If the addition exceeds 10%, or if total non-originating input surpasses 40%, the final product loses preferential origin.

8. Operational Procedure

|

9. Verification and Customs Control

-

Customs authorities may verify origin claims by reviewing:

-

Stock and accounting segregation records;

-

Value calculations for non-originating additions;

-

Supplier origin documentation and statements;

-

Outgoing origin declarations.

-

-

Non-compliance may result in loss of preferential treatment and retroactive duty recovery.

10. Summary Table - Storage Context (HS 2710)

|

11. Conclusion

In storage operations under the EU-UK TCA, the preferential origin of petroleum products (heading 2710) can be maintained provided that:

-

Goods are handled under accounting segregation systems ensuring traceable origin management;

-

Any addition of non-originating materials does not exceed 10% of the ex-works value, and total non-originating input remains within the 40% PSR limit;

-

No operations constitute insufficient working or processing under Article ORIG.7.

By applying these controls, operators can confidently issue Statements on Origin while maintaining full compliance with the TCA's preferential origin framework.

Statement on origin

To be printed on an invoice or commercial document containing information on the goods concerned

SOP - Decision flow Preferential origin EU - UK TCA tariff Heading 2710

Decision flow Preferential origin EU - UK TCA tariff Heading 2710

Template preferential origin (long term) supplier declaration

[TO BE PRINTED ON COMPANY LETTERHEAD]

SUPPLIER'S DECLARATION

I, the undersigned, declare that the goods listed on this document …………………………….……………….(1), originate in ……………………………….(2) and satisfy the rules of origin governing preferential trade with ……………………………………………(3).

I declare that (4):

Cumulation applied with

…………………………………(name country/countries)

Cumulation applied with

…………………………………(name country/countries)

No cumulation applied

No cumulation applied

I undertake to make available to the customs authorities any further supporting documents they require.

……………………………………………………………………….…. (5)

………………………………………………………………………….. (6)

Footnotes (can be removed after completion)

(1) If only some of the goods listed on the document are concerned, they shall be clearly indicated or marked and this marking entered in the declaration as follows:

“………………..…listed on this document and marked …………………..….originate in ………………….…

(2) The European Union, country, group of countries or territory, from which the goods originate

(3) Country, group of countries or territory concerned

(4) To be completed, where necessary, only for goods having preferential origin status in the context of preferential trade relations with one of the countries with which pan-Euro-Mediterranean cumulation of origin is applicable.

(5) Place and date of issue

(6) Name and position of the undersigned, name and address of company

(7) Signature

LONG-TERM SUPPLIER'S DECLARATION

I, the undersigned, declare that the goods described below:

…………………………………………………………………….(1)

…………………………………………………………………….(2)

Which are regularly supplied to ………………………………….(3), originate in ……………………………….(4) and satisfy the rules of origin governing preferential trade with ……………………………………………(5).

I declare that (6):

Cumulation applied with

…………………………………(name country/countries)

Cumulation applied with

…………………………………(name country/countries)

No cumulation applied

No cumulation applied

This declaration is valid for all shipments of these products dispatched from ......................................... to

...............................(7)

I undertake to inform ............................................(3) immediately if this declaration is no longer valid.

I undertake to make available to the customs authorities any further supporting documents they require.

……………………………………………………………………….…. (8)

………………………………………………………………………….. (9)

Footnotes (can be removed after completion)

Footnotes (can be removed after completion)

(1) Description

(2) Commercial designation as used on the invoices e.g. Model No

(3) Name of the company to which goods are supplied

(4) The European Union, country, group of countries or territory, from which the goods originate

(5) Country, group of countries or territory concerned

(6) To be completed, where necessary, only for goods having preferential origin status in the context of preferential trade relations with one of the countries with which pan-Euro-Mediterranean cumulation of origin is applicable.

(7) Give the start and end dates. The period shall not exceed 24 months.

(8) Place and date of issue

(9) Name and position of the undersigned, name and address of company