Non-Preferential origin

It determines a product's "normal" origin under the World Trade Organization (WTO) framework and the Union Customs Code (UCC).

- General principles

- General Procedure: Determination of Non-Preferential Origin

- Case law

- Decision flow non-preferential origin

- Template non-preferential origin (long term) supplier declaration

- Verification of Supplier's Declaration - Non-Preferential Origin

- Issue ITR Declaration of Origin

- Work instruction (commercial incentive)

- Work instruction (simplified process)

General principles

Introduction and Context

1. Meaning of non-preferential origin

Non-preferential origin determines the economic nationality of a product for general customs purposes within the EU. It establishes which country a product is considered to originate from when imported or exported, independently of any preferential trade agreements.

Unlike preferential origin, which is used to access reduced or zero tariff rates under free trade or economic partnership agreements, non-preferential origin is used primarily to:

-

Determine applicable customs duties under the EU Common Customs Tariff;

-

Enforce trade remedies (e.g., anti-dumping, countervailing duties, safeguards);

-

Comply with labelling, marking, or origin-statistics requirements;

-

Support customs control and enforcement of EU trade law.

To establish non-preferential origin, a product must either:

-

Be wholly obtained in one country (e.g., minerals, agricultural products, animals raised, or goods extracted/harvested); or

-

Have undergone substantial, economically justified processing or working in a country that results in a change in tariff classification, physical or chemical properties, or composition, thereby constituting a “substantial transformation.”

These rules ensure that origin determinations reflect the true country of production, prevent circumvention of EU trade rules, and provide legal certainty for customs authorities and economic operators.

2. Purpose of Non-Preferential Origin Procedures

The purpose of establishing and verifying non-preferential origin is to:

-

Ensure accurate application of the EU Common Customs Tariff;

-

Prevent circumvention of customs duties through minimal processing, transshipment, or mislabelling;

-

Support fair competition in the EU market;

-

Provide customs authorities with a verifiable and auditable framework for determining origin;

-

Enable importers and exporters to accurately declare the origin of goods for compliance, enforcement, and trade statistics;

-

Facilitate the application of trade defense measures (anti-dumping, countervailing duties, safeguards) when appropriate.

3. Legal Basis

For the European Union, non-preferential origin is governed by:

-

Articles 148–152 of the Union Customs Code (Regulation (EU) No 952/2013);

-

Delegated and Implementing Acts supplementing the UCC, including Annex 22‑01 and related product-specific rules for non-preferential origin;

-

Customs procedures and national regulations implementing the UCC in Member States;

-

CJEU case law interpreting substantial transformation, minimal operations, and primary rules (e.g., C‑86/24 CS STEEL, C-589/17 Prenatal S.A., C-297/23 Harley-Davidson Europe).

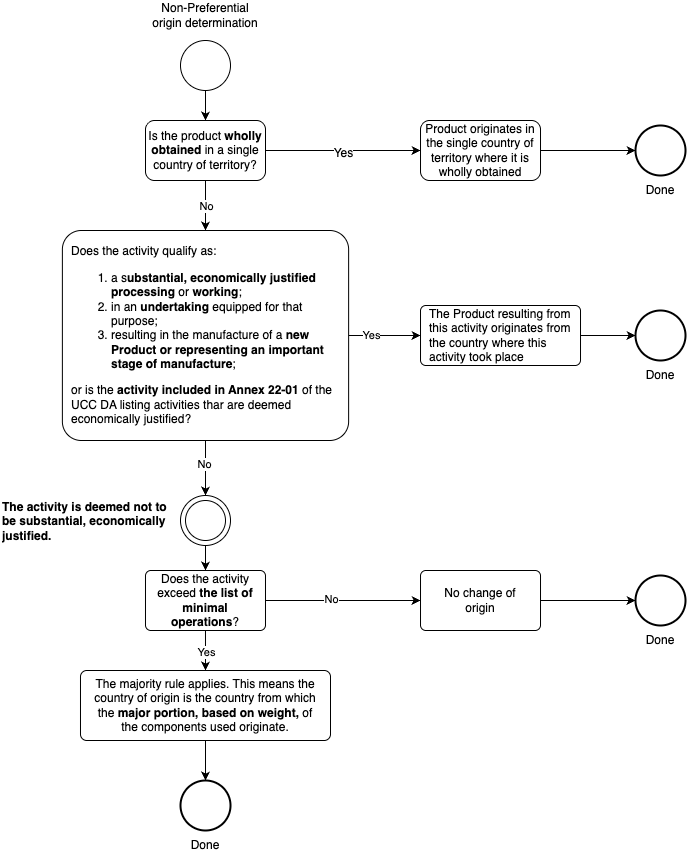

General Procedure: Determination of Non-Preferential Origin

Step 1 - Classify the Goods

Determine the correct HS/CN code of the final product.

Check whether the product is listed in Annex 22‑01 (or other EU codified rules).

Step 2 - Check if Goods Are Wholly Obtained

Confirm extraction, production, or manufacture occurred entirely in one country.

If yes → assign origin to that country; no further steps required.

Step 3 - Identify All Countries of Production/Processing

List all countries involved in the supply chain (raw materials, intermediate products, semi-finished goods).

Step 4 - Assess Substantial Transformation

For each processing step, determine:

Nature of operation (chemical change, assembly, finishing)

Economic justification (not solely for tariff avoidance)

Resulting change (new HS heading, change in physical or chemical properties).

Step 5 - Apply Codified List Rules (if applicable)

Check Annex 22‑01 or equivalent for the HS code.

Verify whether the last operation qualifies as “substantial transformation” under the codified rule.

Step 6 - Apply Residual Rule (if no codified rule applies)

Determine the last economically justified processing or use majority material/value rule to assign origin.

Step 7 - Document All Steps

Record:

-

Input materials, their origin, and HS classification

-

Production steps and locations

-

Processing dates and invoices

-

Evidence of substantial transformation (technical specs, change of properties, quality tests).

-

Step 8 - Declare Origin in Customs Procedure

Include origin in import declaration for free circulation.

Attach supporting documents as requested.

Step 9 - Maintain Records for Audit & Post-Clearance

Retain all documentation for the statutory period (usually 3–5 years).

Be prepared for customs inspection or administrative review.

Case law

|

Decision flow non-preferential origin

Template non-preferential origin (long term) supplier declaration

Suppliers declaration for products of non-preferential origin - Single use

I, the undersigned, declare that the goods listed on this invoice (1) were produced (2).

I undertake to make available to the Chamber of Commerce any further supporting documents they require.

Place and date:

Name and position:

Signature:

- It should be used within the European Union only.

- This declaration is to be placed on the invoice, packing list or other trade document in which the goods are sufficiently specified. This declaration can also be placed on the supplier’s company letter paper. In that case please refer to the

invoice number.

(1) State the number of the invoice or other document in which the shipment is sufficiently specified. The number needs not to be mentioned if the statement is placed on the invoice.

- When instead of the invoice another document or an annex to the invoice is being used, the kind of document concerned shall be mentioned instead of the word ‘invoice’.

- When the statement concerns only part of the goods listed on the invoice, these should be clearly indicated or marked. Furthermore, this marking should be indicated on the declaration as follows: ‘... listed on this invoice and

marked .................... were produced in .................... and...’

(2) State just the applicable option. If products are delivered of EU origin together with products of non-EU origin, various supplier’s declarations should be issued.

(3) State the country of origin (member state of the European Union); if various goods are of different origins, these origins shall be mentioned to each item.

(4) According to Regulation (EU) 952/2013 art. 61 sub 3. (PB L 269 of 10.10.2013).

(5) State the country of origin; if various goods are of different origins, these origins shall be mentioned to each item.

Verification of this declaration by means of a certificate of origin, issued by the supplier’s regional Chamber of Commerce, may be required by the buyer’s regional Chamber of Commerce.

This declaration is not valid for goods having preferential origin status and which qualify for movement certificates EUR.1, EUR-MED or invoice declaration. For such use the “declaration for products having preferential origin status”according to Regulation (EU) 2015/2447 Annex 22-15 (PB L 343 of 29.12.2015) is applicable.

Suppliers declaration for products of non-preferential origin - Regular use

Long-term suppliers declaration for products of non-preferential origin

I, the undersigned, declare that the goods described below (1)(2)

are produced (4)

⃞ in the European Union, namely in according to the Union Customs Code art. 61 sub 3. (6)

⃞ outside the European Union and originate in (5), and satisfy the rules of origin(7).

This declaration is valid for all shipments of these products dispatched from ______ to ________(8).

I undertake to inform ___________(3) immediately if this declaration is no longer valid.

I undertake to make available to the Chamber of Commerce any further supporting documents they require.

Place and date:

Name and position:

Name and address of the company:

Signature:

- This declaration is to be placed on the supplier’s letter paper.

- The LSO should only be used within the European Union.

Notes for completion of the declaration:

(1) Description of the goods.

(2) Trade description as used on invoices, e.g. model No.

(3) Name of buyer.

(4) State just the applicable option. If products are delivered of EU origin together with products of non-EU origin, various suppliers declarations should be issued.

(5) State the country of origin (member state of the European Union); if various goods are of different origins, these origins shall be mentioned to each item.

(6) According to Regulation (EU) 952/2013 art. 61 sub 3. (PB L 269 of 10.10.2013).

This declaration is not valid for goods having preferential origin status and which qualify for movement certificates EUR.1, EUR-MED or invoice declarations. For such use the “declaration for products having preferential origin status” according to Regulation (EC) 2015/2447, art. 62, annex 22-16 (PB L 343 of 29.12.2015) is applicable.

Verification of Supplier's Declaration - Non-Preferential Origin

Purpose

To ensure that supplier declarations claiming non-preferential origin are accurate, legally compliant, and auditable for EU customs purposes.

Step 1: Collect the Supplier Declaration

-

Obtain a completed supplier declaration for all goods, including:

-

Product description and Commodity code.

-

Country of origin.

-

Basis of origin (wholly obtained or substantially transformed).

-

Signature, company details, and date.

-

-

Ensure the declaration is dated, legible, and signed by an authorized representative.

Step 2: Verify Supplier Credentials

-

Confirm the supplier is legitimate and traceable.

-

Check:

-

Legal registration of the supplier.

-

Manufacturing locations.

-

Historical compliance with customs documentation.

-

Step 3: Check Completeness of the Declaration

-

Ensure all required fields are completed:

-

Product description matches your purchase.

-

Commodity code matches the EU customs classification.

-

Country of origin is stated.

-

Basis of origin (wholly obtained/substantial transformation) is clear.

-

Declaration is signed and dated.

-

Step 4: Validate Basis of Origin

-

For wholly obtained goods:

-

Confirm that all production, extraction, or harvest occurred in the stated country.

-

Request supporting documentation if necessary (e.g., harvest records, production logs).

-

-

For substantially transformed goods:

-

Confirm that processing in the stated country was economically justified and resulted in a substantial transformation:

-

Check change in tariff classification (Commodity code).

-

Check change in physical/chemical properties or composition.

-

Ensure processing was more than minimal operations (not just cleaning, packaging, sorting).

-

-

Step 5: Check Supporting Evidence

-

Review:

-

Invoices for raw materials.

-

Production or processing logs.

-

Bills of lading.

-

Quality certificates or process descriptions.

-

-

Ensure consistency between documentation and the declaration.

Step 6: Cross-Check Against Legal Requirements

-

Verify compliance with:

-

UCC Articles 148-152 (non-preferential origin rules).

-

Delegated / Implementing Acts (Annex 22-01, list of primary rules, minimal operations).

-

-

Ensure the declared origin aligns with EU customs rules and relevant CJEU case law (e.g., C-86/24 CS STEEL).

Step 7: Approve or Request Clarification

-

If all criteria are satisfied:

-

Approve the declaration for use in customs procedures.

-

-

If inconsistencies are found:

-

Contact supplier to provide additional information or correct the declaration.

-

-

Keep all correspondence for audit purposes.

Step 8: Record Retention

-

Retain the supplier declaration and all supporting documents for at least 3-5 years (EU standard for customs audits).

-

Store in a retrievable format (electronic or paper) linked to the relevant shipment.

Step 9: Periodic Review

-

Review supplier declarations periodically (at least annually) to:

-

Confirm consistency with current supply chains.

-

Ensure compliance with updates to UCC or Delegated Regulations.

-

Flag changes in production location or processing steps that may affect origin.

-

This procedure ensures that your non-preferential origin declarations are reliable, auditable, and legally defensible in case of customs verification or post-clearance checks.

Issue ITR Declaration of Origin

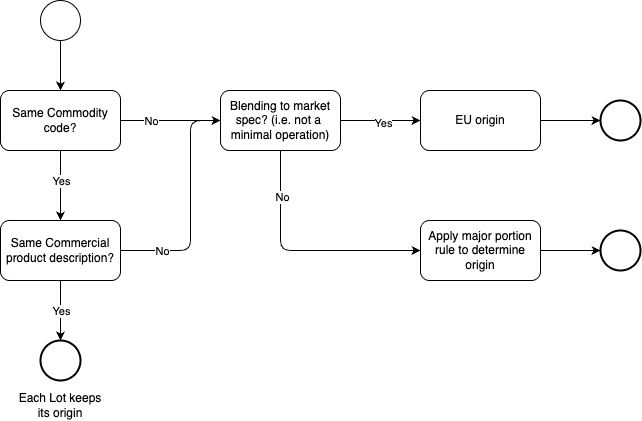

The declaration of origin (DoO) report is produced from the terminal operating system and provides an overview of the breakdown of the components and administrative lots that were included in the blending operations. Origin determination is based on the DoO.

Work instruction (commercial incentive)

In practice, there are two types of documents that refer to non-preferential origin:

An official Certificate of Origin (CoO), which exporters can obtain by applying to the competent Chamber of Commerce or the relevant customs authorities; and

A commercial document declaring the non-preferential origin (Terminal Origin Declaration).

Upon request, our terminal can assist with the application for the relevant certificate or document via a broker authorised to apply for an official CoO (digital connection required). When applying with the Chamber of Commerce the burden of proof is greater than when issuing a Terminal Origin Declaration, because the latter is not an official document and it is the discretion of the Terminal to conclude on origin and the proof that is provided. For example, when documentation is provided that the Product comes from a refinery in Italy the Terminal may be inclined to accept this as sufficient proof, where the Chamber of Commerce is likely to require a Suppliers declaration for non-Preferential origin. Apart from whether or not the proof of origin for the components is sufficient or not, the procedure in determining the origin should be the same with the terminal itself and the Chamber.

As this involves blending rather than mere storage, the major portion rule applies, provided that customers inform us of the origin and substantiate it with appropriate documentation. This requirement applies at least to the parcel representing the major portion based on weight. The origin of the remaining parcels may be unknown without affecting this assessment.

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.096.530 | 45.579.910 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

| Blended product | ||||||

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.341.424 | 45.929.758 |

The processed product results from the combination of several significant components. The fact that one of these components shares the same Commodity code as the final product does not alter this assessment. In quantitative terms, it is not considered a “base” product to which only minimal operations are applied. Accordingly, a new product is deemed to have been created. The majority of the product is not RON 95. The process here is to get the RON 91 to a RON 95 making it a process to obtain a Product by deliberate and proportionate blending.

Components | ||||||

Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

T x | Gasoline RON 91 | 2710 1241 90 | T1 - Bonded | Norway | 28.077.224 | 36.463.928 |

T x | Naphta | 2710 1225 90 | T1 - Bonded | Unknown | 5.565.992 | 7.951.417 |

T x | Alkylate | 2710 1290 90 | T2 - Excise controlled | Unknown | 4.634.938 | 6.019.400 |

T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Unknown | 17.670.712 | 22.948.977 |

T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

Blended product | ||||||

T x | Gasoline RON 95 | 2710 1245 90 | T1 - Bonded | EU/Netherlands | 56.193.763 | 73.733.571 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | IMFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | Cutterstock | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T1 - Bonded | EU/Netherlands | 54.743.046 | 54.915.871 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

Work instruction (simplified process)

In practice, there are two types of documents that refer to non-preferential origin:

An official Certificate of Origin (CoO), which exporters can obtain by applying to the competent Chamber of Commerce or the relevant customs authorities; and

A commercial document declaring the non-preferential origin (Terminal Origin Declaration).

Upon request, our terminal can assist with the application for the relevant certificate or document via a broker authorised to apply for an official CoO (digital connection required). When applying with the Chamber of Commerce the burden of proof is greater than when issuing a Terminal Origin Declaration, because the latter is not an official document and it is the discretion of the Terminal to conclude on origin and the proof that is provided. For example, when documentation is provided that the Product comes from a refinery in Italy the Terminal may be inclined to accept this as sufficient proof, where the Chamber of Commerce is likely to require a Suppliers declaration for non-Preferential origin. Apart from whether or not the proof of origin for the components is sufficient or not, the procedure in determining the origin should be the same with the terminal itself and the Chamber.

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.096.530 | 45.579.910 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

| Blended product | ||||||

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Norway | 35.341.424 | 45.929.758 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | Gasoline RON 91 | 2710 1241 90 | T1 - Bonded | Norway | 28.077.224 | 36.463.928 |

| T x | Naphta | 2710 1225 90 | T1 - Bonded | Unknown | 5.565.992 | 7.951.417 |

| T x | Alkylate | 2710 1290 90 | T2 - Excise controlled | Unknown | 4.634.938 | 6.019.400 |

| T x | Gasoline RON 95 | 2710 1245 90 | T2 - Excise controlled | Unknown | 17.670.712 | 22.948.977 |

| T x | Additive | 3811 1900 90 | T2 - Excise controlled | Unknown | 244.894 | 349.849 |

| Blended product | ||||||

| T x | Gasoline RON 95 | 2710 1245 90 | T1 - Bonded | Unknown | 56.193.763 | 73.733.571 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | RMK 500 | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | IMFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | Cutterstock | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 54.743.046 | 54.915.871 |

| Components | ||||||

| Tank | Product | Commodity code | Status | Origin | Kilogram | Liters 15 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 5.565.992 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |

| Blended product | ||||||

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 427.486 | 429.112 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 243.967 | 244.894 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 4.617.392 |

| T x | HSFO | 2710196800 | T2 - Excise controlled | Unknown | 4.634.938 | 5.587.141 |

| T x | HSFO | 2710196800 | T1 - Bonded | Malaysia | 43.870.663 | 44.037.332 |