Mercosur

- Introduction

- End-use

- Ethanol passage - Annex 2 Tariff Elimination Schedule Section A

- Validity Import license

- Classification

- End use license

Introduction

From that date, tariff preferences and TRQs, including those for ethanol originating in Brazil, are intended to become legally applicable under the provisional application mechanism of Article 218(5) of the Treaty on the Functioning of the European Union.

However, actual use in practice still depends on the scope of the Council Decision and EU implementation measures, including TARIC activation and any conditions attached to the ethanol quota (e.g. industrial end-use or administrative controls). Only measures explicitly included in the provisional application package can be used from day one.

In short: ethanol imports from Brazil are covered in principle from 1 May 2026, but their practical availability depends on final EU implementation and system activation.

(6) The Council, on a proposal by the negotiator, shall adopt a decision concluding the agreement.

Except where agreements relate exclusively to the common foreign and security policy, the Council shall adopt the decision concluding the agreement:

- after obtaining the consent of the European Parliament in the following cases:

- association agreements

- agreement on Union accession to the European Convention for the Protection of Human Rights and Fundamental Freedoms

- agreements establishing a specific institutional framework by organising cooperation procedures

- agreements with important budgetary implications for the Union

- agreements covering fields to which either the ordinary legislative procedure applies, or the special legislative procedure where consent by the European Parliament is required

The European Parliament shall be immediately and fully informed at all stages of the procedure.

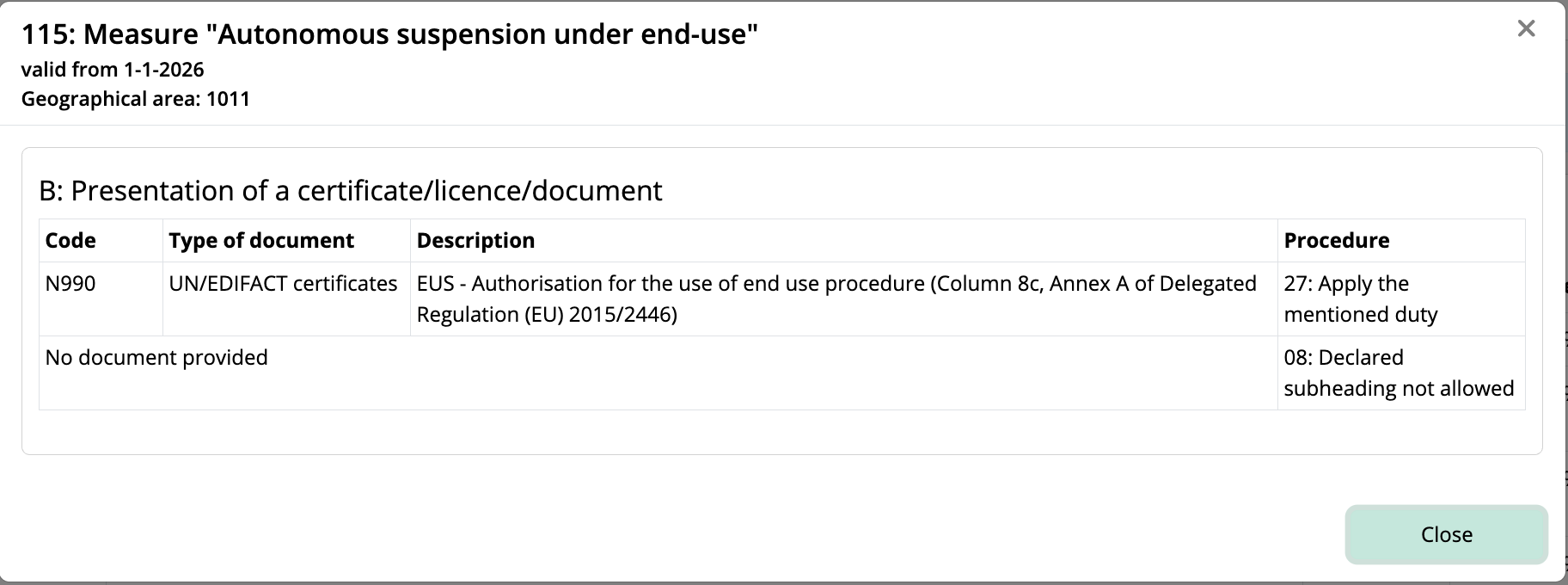

End-use

The “end-use” reference in the EU–Mercosur ethanol TRQ should be understood as an agreement-level tariff condition (intended use requirement) and not, as such, the EU customs end-use special procedure under the Union Customs Code (including Article 211 UCC). In practical terms, this means you are not automatically required to apply for or operate under a customs end-use authorisation system solely because of this wording. Your immediate obligation is to ensure that, if and when the chemical-industry TRQ is claimed, you can demonstrate and document downstream delivery to bona fide industrial users in CN Chapters 28–40, supported by contractual end-use declarations and traceable sales and delivery records. Only if the EU were to formally implement a separate customs end-use procedure under UCC rules would a licensing requirement under Article 211 potentially become relevant.

Ethanol passage - Annex 2 Tariff Elimination Schedule Section A

21. Tariff rate quota for ethanol

(a) Originating goods marked with the notation "TRQ-EL" in Appendix 2-A-1 and listed in point (d) shall be subject to the in-quota tariff rate in point (b) of this paragraph in the following years and aggregate quantities, except for a duty-free portion of the total aggregate quantity in each year being reserved for a specific use for the chemical industry1:

Year | Aggregate annual quantity (MT) All uses | Aggregate annual quantity (MT) Specific use: for the chemical industry | Total aggregate annual quantity (MT) |

0 | 33 333 | 75 000 | 108 333 |

1 | 66 667 | 150 000 | 216 667 |

2 | 100 000 | 225 000 | 325 000 |

3 | 133 333 | 300 000 | 433 333 |

4 | 166 667 | 375 000 | 541 667 |

5 and each subsequent year | 200 000 | 450 000 | 650 000 |

1 The EU may provide that imports of ethanol under the portion of the quota reserved for use by the chemical industry are subject to an End Use Procedure, with a view of conducting the customs control relating to the use of such goods. The objective is to ensure that those imports are used for manufacturing products classified under Chapters 28 to 40 of the EU Combined Nomenclature (CN). The customs controls applied to prevent circumvention of imports into the fuel or beverage market shall not represent a burden beyond those measures necessary to control imports under this TRQ. Those measures shall be proportional to the risk of circumvention and their urgency and shall be taken in accordance with Articles 4.12 and 4.16, inter alia considering the record of the importer as appropriate.

(b) For the quota for all usages the in-quota duty for the undenatured ethyl alcohol imported under subheading 2207.10 and tariff items 2208.90.91 and 2208.90.99 shall be 6,4 (six point four) EUR/hl, and the in-quota duty for the denatured ethyl alcohol imported under subheading 2207.20 shall be 3,4 (three point four) EUR/hl. For the quota for specific use for the chemical industry the in-quota duty shall be 0 (zero).

(c) Originating goods entered in excess of the aggregate quantities set out in point (a) of this paragraph shall be subject to the base rate of the customs duty set out in Appendix 2-A-1.

(d) This paragraph applies to originating goods classified in the following tariff items: 2207 10 00, 2207 20 00, 2208 90 91 and 2208 90 99.

Validity Import license

For an AGRIM import licence (L001), the relevant EU import licensing rules (including Delegated Regulation (EU) 2016/1237 and Implementing Regulation (EU) 2016/1239) provide that the import declaration can only be validly made by:

- the holder of the licence (titular), or

- the transferee (cessionary), or

- a customs representative acting on behalf of either of the above.

This means that the terminal, acting in its own name but on behalf of the importer, becomes the declarant and assumes joint liability towards the customs authorities together with the importer of record, including responsibility for compliance with the licence conditions and any resulting customs debt.

Classification

End use license