Definitions used in Customs process flows

What is considered a Blend from a customs perspective?

To determine what customs procedure must be applied in relation to operational activities, whereby two or more Products are mixed together, it is important to understand what is defined as a mixture or, in case of fluid Products, a Blend. In the area of customs, there are two main processes that allow for the avoidance of import duties becoming payable or taxes, such as excise duties, becoming due. This is the Process of Storage and Manufacturing/Processing.

To be able to suspend import duties or taxes, what licenses are required depends on the customs status and types of Products. The customs statuses are non-Union (T1, Bonded) and Union (T2, Domestic). In relation to T2 Products, local taxes may be applicable such as excise duties (or other consumption taxes). When Products are qualified as Excise Product they may be under certain control measures to ensure the appropriate taxation of these products. These type of Products are referred to as Excise controlled. When Products are of the T2 customs status and no local tax control apply, the type of Products are referred to as Domestic (Free).

For further details kindly have a look at:

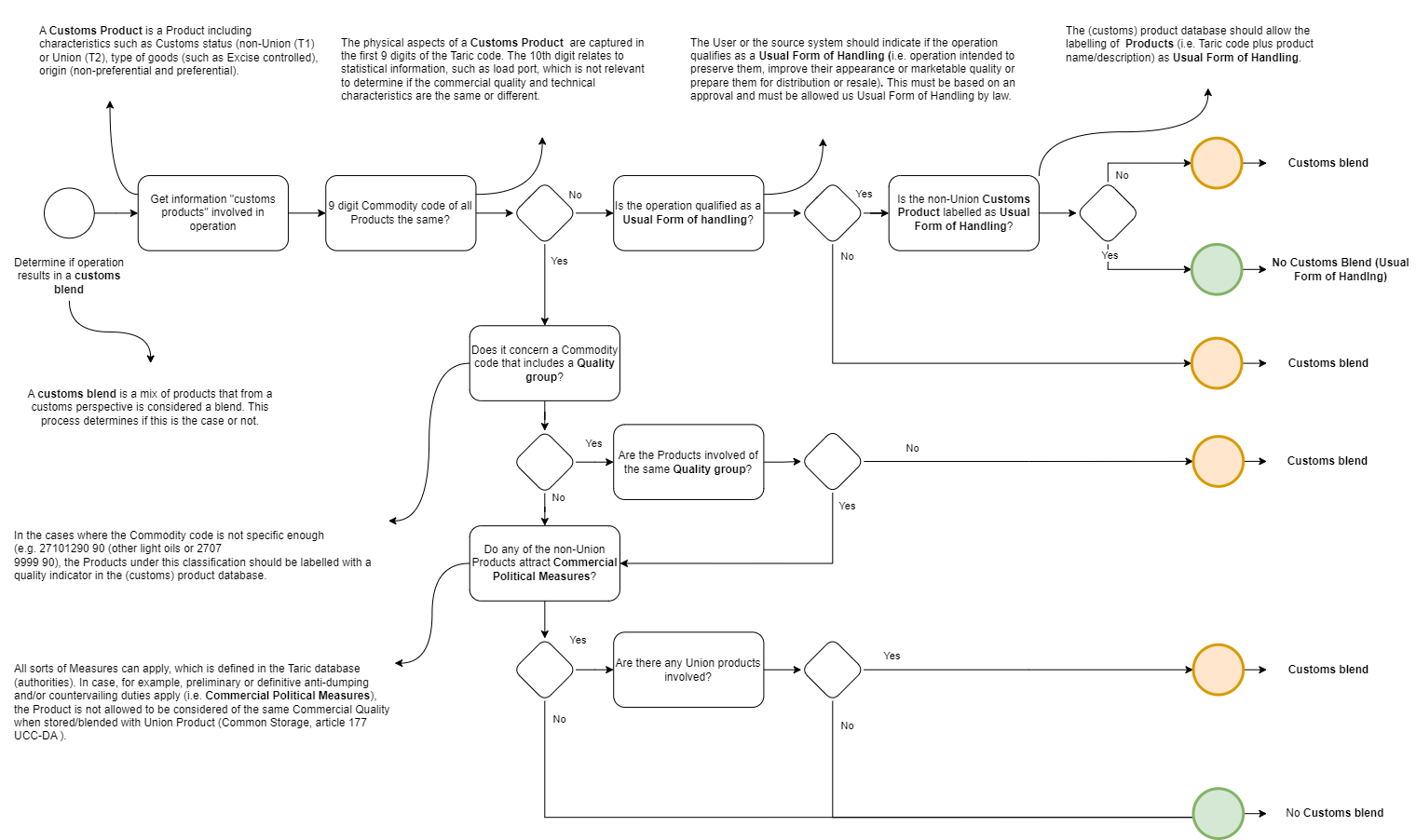

When talking about a mixture, or blend, it is important to take the above elements into consideration. Below a Process flow of the steps to determine if, in the Energy Products industry, an operational activity results in a Customs Blend.

Customs status and Type of Products

The legislation defines Union goods in article 5, paragraph 23, UCC. Products with the non-Union customs status are referred to as any Product NOT of the Union customs status (article 5, paragraph 24, UCC). Inherent to the definition is that in case Product of the Union status are mixed with non-Union goods, the Product no longer meets the criteria of Union good and hence 'loses its customs status'.

Product can lose its Union customs status when placed under a customs procedure insofar the law allows it (article 154, sub b, UCC)