Customs valuation procedure

This document contains a description of VTTI's procedure applied at the terminals for determining the customs value of goods.

Scope and purpose

This Customs Valuation Procedure sets out the principles, scope, and practical steps applied by VTTI for determining the customs value of goods imported into the European Union.

The purpose of this document is to ensure that customs values are established in a consistent, accurate, and compliant manner, in line with the requirements of the UCC and related legislation. It aims to provide clear guidance to relevant personnel on how to determine the appropriate valuation method, perform the necessary checks, and document the outcome of the valuation process.

This procedure applies to all imports of goods into the EU where VTTI is involved in the declaration process, regardless whether that declaration is filed under (in)direct customs representation or on behalf of VTTI itself. It covers, in detail:

the selection of the appropriate customs valuation method;

the application of the selected customs valuation method;

the identification of elements to be added to or excluded from the customs value;

the verification steps required to ensure the accuracy and completeness of the declared value; and

the documentation and record-keeping requirements supporting the declared customs value.

This procedure serves as a practical reference for personnel involved in customs declarations and should be followed when determining and reviewing customs values for import into the EU.

Risk and responsibility

When it comes to the allocation of risk and responsibility for customs valuation, a distinction should be made between the private law and the public law perspective.

From a public law perspective, pursuant to Article 15 of the Union Customs Code, VTTI bears responsibility towards the customs authorities for the accuracy and completeness of the information contained in any customs declaration it lodges and the authenticity, accuracy and validity of any document supporting the declaration, regardless of whether that declaration is submitted in its own name or on behalf of a customer under customs representation.

From a private law perspective, responsibility for timely providing the documentation and information necessary for the customs declaration rests with the customer. As VTTI is not the owner of the goods declared for import, it has only limited visibility of the underlying supply chain, transactions, and parties involved. VTTI therefore relies on the information provided by the customer. This reliance is reflected in the

general terms and conditions applicable between VTTI and its customers, which confirm that, in their mutual relationship, the customer is responsible for the availability and accuracy of such information.

From a practical perspective, this results in a cooperation between VTTI and the customer in relation to customs valuation. The customer provides VTTI with the relevant information, after which CS performs certain predefined sanity and reasonableness checks and follows up with the customer in case of doubt or apparent inconsistencies before lodging the import declaration.

Methodology selection

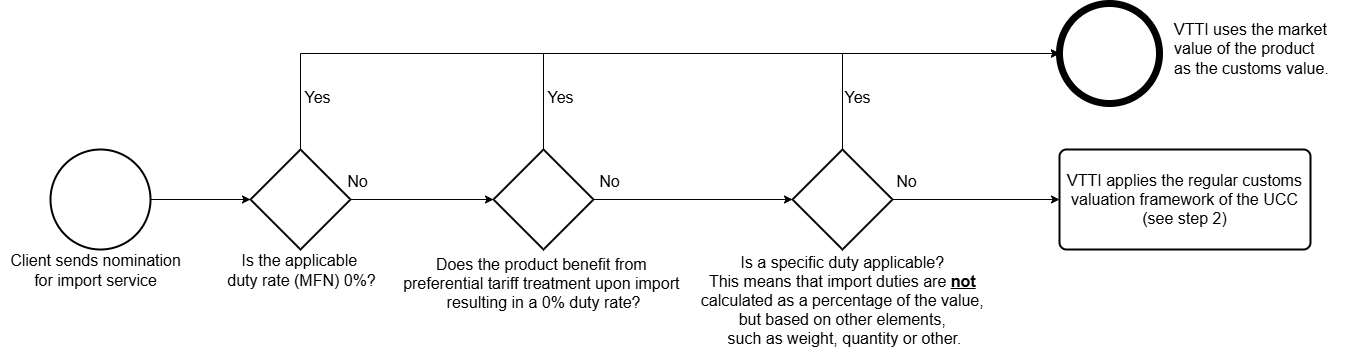

Step 1: Assess if pragmatic approach may be applied

The Dutch Customs Authorities have agreed that VTTI may use the market value of a product as the customs value in the import declaration in situations where the customs value has no impact on the amount of duties payable. First step in the valuation procedure is to determine whether this pragmatic approach can be applied.

When a product arrives at the terminal and a parcel is registered in ERP, the value of the product is recorded by CS in line with the market value at the time of registration. The market value is usually provided by the customer, or otherwise obtained by CS from publicly available market data sources.

When the customer sends a nomination to bring the product into free circulation, CS registers an import service in ERP. The import service requires a value, which is used in the import declaration.

Where the applicable import duty rate is 0%, the goods qualify for preferential treatment upon import, or where a specific duty applies (i.e., duties are not calculated over the value but over another factor such as weight), the customs value declared serves a purely statistical purpose and has no financial impact. In such cases, the customs authorities have approved that VTTI applies the “reasonable means” method as an alternative method of customs valuation, in accordance with Article 74(3) of the UCC. More specifically, the market value that was registered at the time the parcel was created is used as the customs value in the import declaration.

If the import duty rate exceeds 0%, no preferential treatment applies and customs duties due are calculated on an ad valorem basis, the regular customs valuation framework of the UCC will be applied to determine the customs value.

This approach can be schematically displayed as follows:

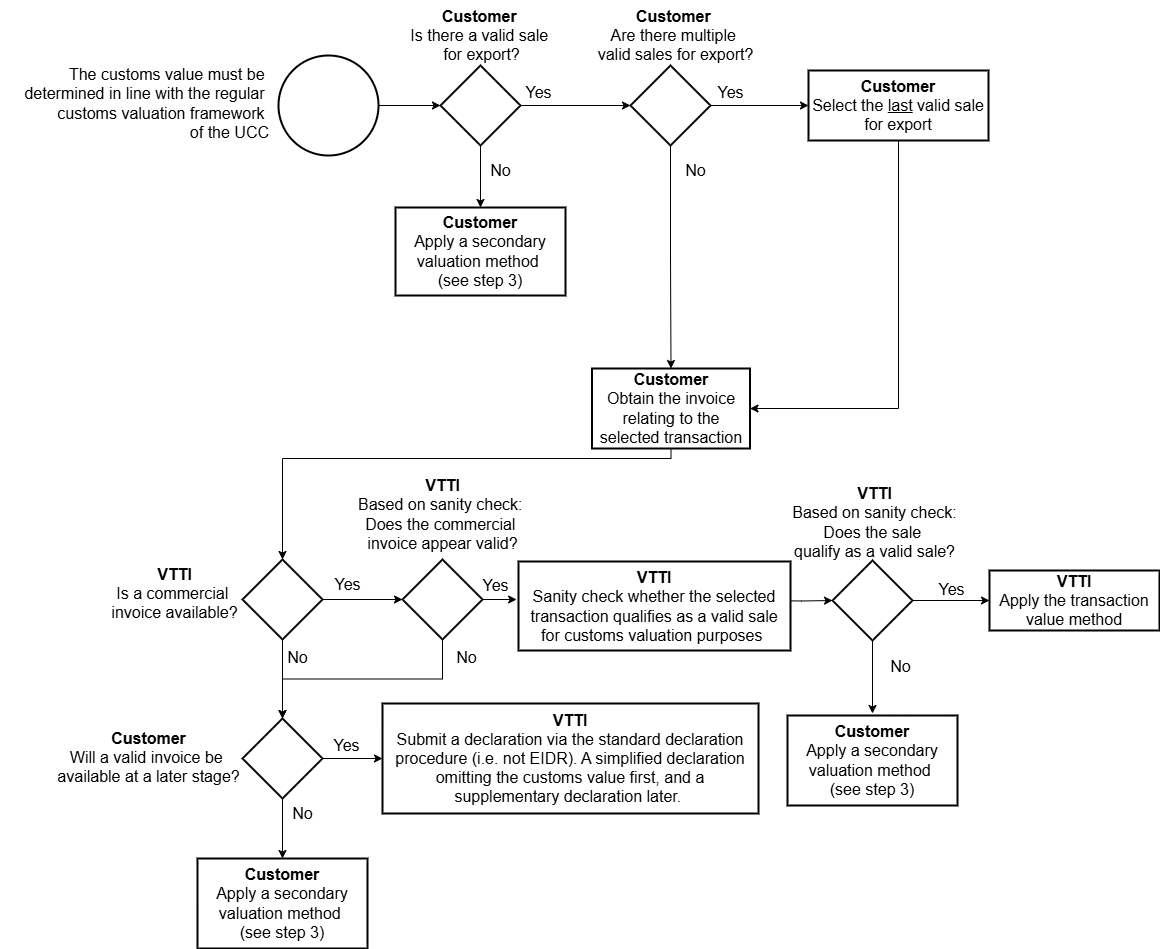

Step 2: Assess applicability of transaction value method

If Step 1 results in the customs value being determined under the regular customs valuation framework of the UCC, the next step is to assess whether the transaction value method can be applied. As this is the primary customs valuation method, the assessment should determine whether the method is available and, if so, which transaction forms the basis for the customs value. The assessment framework is set out below.

Step 2.1: Identification of a qualifying sales transaction

The transaction value method can only be applied if the goods are sold for export to the EU. This means that ownership of the product is transferred from the seller to the buyer, and that, at the time of the sale, it is clear that the product is intended for export to the EU.

If the product is not sold prior to its physical entry into the EU, but while in temporary storage, under external transit, in a customs warehouse or under inward processing, such a sale may also qualify as a "sale for export" on which the transaction value can be based.

If the product is sold multiple times prior to its arrival in the EU (i.e., more than one sale qualifies as "sale for export"), the transaction value must be based on the last sale, i.e. the sale concluded immediately before the goods enter the EU.

As VTTI has limited insight in the supply-chain and the underlying transactions, the customer indicates whether or not a sale for export exists and which sale qualifies as the last sale for export. The customer provides CS with the relevant information regarding that sale, including the commercial invoice.

If the customer indicates that no sale for export exists, the value must be determined in line with one of the secondary valuation methods, briefly described below under step 3. This scenario is extremely rare in the energy products market.

Step 2.2: Review of the commercial invoice

The commercial invoice which relates to the declared transaction value is required as a supporting document. It is the responsibility of the customer to provide CS with a valid commercial invoice. CS performs a sanity check on the invoice.

In exceptional cases, where a final commercial invoice is not available, alternative supporting documents (such as a pro forma invoice, “for customs purposes only” invoice, or other preliminary invoice) may be accepted, provided that they accurately reflect the transaction value and this value can be substantiated by the underlying commercial documentation. CS will consult the customs specialists at the terminal or VTTI HQ before using such alternative supporting document for customs valuation.

In case it can be concluded from the sanity check that the invoice appears valid, CS will proceed to step 2.3 as described below. Otherwise, CS will reach out to the customer to discuss findings.

If it appears that no valid invoice is available, the transaction value method cannot be applied. CS will then proceed to step 3.

Step 2.3: Assessment whether the transaction value method can be applied

Following a successful conclusion of the sanity check in step 2.2, CS will accept the invoice. If CS has no access to the commercial invoice relating to the transaction, and the customer can also not provide that invoice at a later stage, the transaction value method cannot be applied and a secondary valuation method must be selected (see step 3). This scenario is extremely rare.

If CS does not have access to the commercial invoice relating to the relevant transaction, but the customer is able to provide the invoice at a later stage, CS will submit a simplified customs declaration in accordance with Article 166 UCC using a provisional customs value based on the information available at the time of importation. Once the invoice becomes available, CS will determine the final customs value in accordance with the transaction value method and submit a supplementary declaration pursuant to Article 167 UCC.

A sale cannot be considered a valid transaction for valuation purposes in the following situations:

Restrictions on use or resale - If the buyer is restricted in how they can use or resell the goods, except for standard restrictions (e.g. legal requirements, geographical resale limits, or restrictions that do not affect the value of the goods).

Price depends on unclear conditions - If the agreed price is influenced by conditions or arrangements for which no clear value can be determined (for example: unknown future compensations, or non-quantifiable obligations).

Proceeds flow back to the seller - If the seller receives (directly or indirectly) part of the proceeds from the buyer’s resale or use of the goods, and this cannot be properly adjusted in the customs value.

Relationship influences the price - If the buyer and seller are related and there are indications that this relationship has affected the agreed price.

As VTTI has limited insight in the supply-chain, the underlying chain of transactions and the contractual circumstances surrounding the sale, it is the responsibility of the customer to assess whether the sale is valid for customs valuation purposes. CS performs a sanity check based on the information available.

The sanity checks conducted by CS are incorporated in a checklist in BzCtrl and included here.

If the sanity check raises any doubt regarding the acceptability of the invoice price, CS will contact the customer to obtain clarification before lodging the declaration.

Step 2 can be schematically displayed as follows:

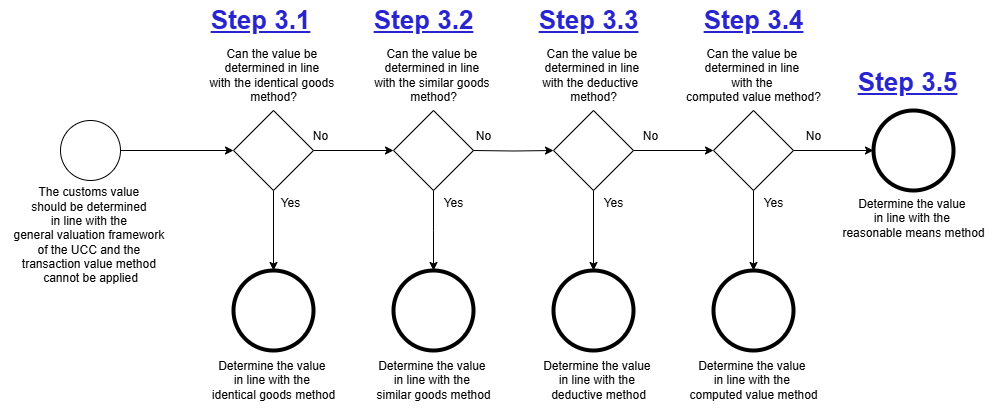

Step 3: Assess applicability of secondary valuation methods

Once it is clear that the customs value must be determined in line with the regular customs valuation framework of the UCC, and its clear that the transaction value method cannot be applied, next step is to assess which of the secondary valuation methods can be applied. In this respect, the following hierarchy must be followed:

Step 3.1: assessment of identical goods method

If possible, the customs value must be based on the transaction value of identical product sold for export to the EU and exported at or about the same time as the product being valued.

In practice, in the supply chains in which VTTI is involved, it is never possible to apply this method, as there is hardly ever such a transaction of identical product available at or about the same time as the product being valued, or the data of that transaction is not available. As such, this secondary valuation method is in practice never applied.

Step 3.2: assessment of similar goods method

If the identical goods method cannot be applied, the customs value should be based on the transaction value of similar product sold for export to the EU and exported at or about the same time as the product being valued.

In practice, in the supply chains in which VTTI is involved, it is never possible to apply this method, as there is hardly ever such a transaction of similar goods available at or about the same time as the goods being valued, or the data of that transaction is not available. As such, this secondary valuation method is in practice never applied.

Step 3.3: assessment of deductive method

If the similar goods methods cannot be applied, the value must in principle be based on the deductive method. The UCC allows for the computed value method to be applied first upon request; however, VTTI does not make use of this option.

Under the deductive method is based on the unit price at which the imported product, or identical or similar imported product, is sold within the customs territory of the Union in the greatest aggregate quantity to persons not related to the sellers. In the supply chains in which VTTI is involved, it is hardly ever possible to apply this method, as VTTI almost never has access to the data required for this valuation method.

Step 3.4: assessment of computed value method

If the deductive method cannot be applied, the customs value should be based on the Computed value method. Under the computed value method, the customs value is calculated as the sum of:

The cost or value of materials, fabrication and other processing employed in producing the imported goods,

An amount for profit and general expenses equal to that usually reflected in sales of goods of the same class or kind as the goods being valued which are made by producers in the country of export for export to the Union and

The cost of transport and insurance and loading and handling charges associated with the transport of the imported product, up to the place where the product is brought into the customs territory of the EU.

Same as with the former secondary valuation methods, it is hardly ever possible to apply this method, due to a lack of data.

Step 3.5: assessment of reasonable means method

If none of the former secondary valuation methods can be applied, the customs value should be determined in line with the reasonable means method. Under this method, the value should be determined on the basis of data available in the customs territory of the EU, using reasonable means consistent with the principles and general provisions of WTO legislation and the UCC. Chapter 5 contains a description of value determination under the reasonable means method.

Conclusion step 3

In conclusion, where the customs value must be determined in accordance with the standard valuation framework of the UCC and the transaction value method cannot be applied, CS will, together with the customer, explore at a high level whether the identical goods, similar goods, deductive or computed value method may be applied. However, based on experience, and given the nature of the liquid bulk industry as well as VTTI’s role in the supply chain, it is in practice rarely possible to apply any of these methods. Consequently, the fallback (“reasonable means”) method will generally be applied.

Where it is determined, following alignment with the customer, that one of the alternative methods can be applied, CS will agree with the customer how that method is to be applied in practice. This will be documented by CS in a client-specific work instruction.

Step 3 can be schematically displayed as follows:

Application of the transaction value method

Once it has been established in the previous section of this procedure that the transaction value method applies, the next step is to determine the customs value accordingly, in accordance with the procedure described on this page.

Price paid or payable

The transaction value is the price actually paid or payable for the goods, in the transaction as selected in the previous section.

In most cases, the price paid or payable is equal to the price mentioned on the commercial invoice provided by the customer. In theory, it might be possible that other payments are made by the buyer to the seller that qualify as "price actually paid or payable for the goods", that are not included in the price mentioned on the commercial invoice. However, this is not common in the liquid bulk sector. CS will monitor if there are signals that such separate amounts paid or payable are applicable. This can for example be the case if the price mentioned on the commercial invoice deviates more than 5% from the current market price. See a more detailed description of this standard check in the previous section of this procedure.

If any amounts are paid or payable for the goods that are not included in the price stated on the commercial invoice, CS will request supporting documentation for those payments and include them in the customs value.

Elements to be added

Certain cost elements may need to be added to the invoice price. These elements are mentioned in Article 71 UCC. VTTI has agreed with its customers that, if such elements are applicable, the customer will in principle notify CS. CS will perform a sanity check to identify any signals that such elements may have been overlooked. Specifically, CS will monitor whether there are indications that one of the following elements applies:

- transport and insurance costs up to the point where the goods enter the EU customs territory, to the extent not already included in the invoice price (In practice, this is an Incoterm check: the CIF price to the point of EU entry should be included. If the Incoterm applied deviates, CS will make adjustments to ensure that costs for transport and insurance up to the point of EU entry are included in the customs value);

- loading and handling charges related to the transport of the goods prior to import;

- commissions or brokerage fees (excluding buying commissions), where relevant for the transaction;

- royalties or licence fees that the buyer must pay as a condition of sale of the goods; and

- any part of the proceeds from the subsequent resale or use of the goods that accrues to the seller.

CS will update the customs value in accordance with any findings under this paragraph. Substantiating documentation and correspondence with the customer will be archived by CS.

Elements to be subtracted

In contrast to the previous paragraph, certain elements must not be included in the customs value where they are already included in the invoice price. These elements are set out in Article 72 UCC. VTTI has agreed with its customers that, where such elements are included in the price on the commercial invoice, the customer will in principle specify these separately, and provide supporting documentation substantiating those elements. CS will perform a sanity check to identify any signals that such elements may not have been correctly excluded. Specifically, CS will monitor whether there are indications that one of the following elements is included in the invoice price:

- transport costs incurred after the goods have entered the EU customs territory (e.g. inland transport beyond the port of entry);

- interest charges related to financing arrangements for the purchase of the goods, provided these are separately identifiable and meet the applicable conditions;

- buying commissions paid by the buyer to its agent;

- import duties, taxes or other charges payable within the EU as a result of the importation or sale of the goods; and

- payments for distribution or resale rights that are not a condition of the sale for export to the EU.

CS will update the customs value in accordance with any findings under this paragraph. Substantiating documentation and correspondence with the customer will be archived by CS.

Application of the reasonable means method

In practice, it is virtually never the case that the customs value cannot be determined using the pragmatic approach or the transaction value method as described earlier in this procedure. Nevertheless, to ensure completeness and robustness of this procedure, an alternative approach has been defined for the exceptional event that such a situation would arise. In such cases, CS will determine the customs value using the reasonable means method, in accordance with article 74, paragraph 3 UCC.

In such cases, CS will base the customs value on the market value of the product, as reflected in the S&P Platts database. Given the nature of the liquid bulk industry, values derived from such price reporting agencies represent the most reliable and objectively verifiable data available. In practice, values determined in this way are generally aligned with, or very close to, the values that would have been established under the other valuation methods.

CS will retain an extract of the relevant database at the time of valuation to ensure that the determined customs value can be properly substantiated towards authorities and other stakeholders.