Customs essentials

Origin

Introduction

In the EU we recognize 2 different types of origin:

- Preferential origin

- Non-preferential origin

Subject to all conditions being met, preferential origin result in the payment of a reduced or nil import duty rate upon import into the EU.

Non-preferential origin does not have an impact on the applicable import duty rate. It can impact the duty amount payable at import as anti-dumping duties and countervailing duties can become due depending on the product and its non-preferential origin. Non-preferential origin also plays a crucial role in relation to sanctions such as import bans. The import ban on certain Russian oils applies when such oil is of non-preferential Russian origin.

It is important to keep in mind that the EU origin rules apply upon import into the EU. If a product has a certain origin based on the EU origin rules, this doesn't automatically mean that it has the same origin when importing into The UK for example. In order to understand the relevant origin of a product, the origin requirements of the country of importation need to be analyzed.

Non-Preferential origin

Non-preferential rules of origin

There are 3 rules that determine the non-preferential origin of a product. The 3rd rule is a residual rule that applies if rule 1 and rule 2 do not apply.

Rule 1

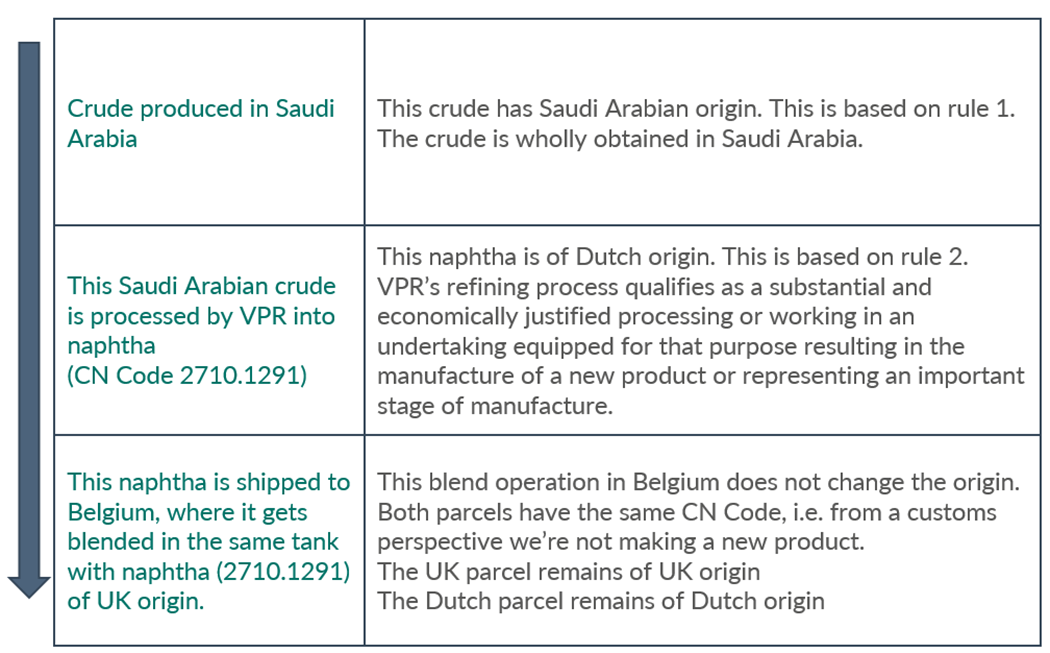

Goods are of non-preferential origin in the single country or territory where these goods are wholly obtained. This reference to country or territory includes territorial waters. It also includes the seabed or subsoil beneath the seabed to which a country has exclusive exploitation rights.

Some examples:

- Crude produced in the USA is of USA origin

- Crude produced outside The UK, from seabed or subsoil beneath the seabed to which The UK has exclusive exploitation rights, is of UK origin

- Diesel produced in Norway out of crude of Norwegian origin is of Norwegian origin under this rule as the product is wholly obtained in a single country

Rule 2

Rule 2 applies to goods produced in more than 1 country or territory.

Goods originate in the country or territory in which

- they underwent their last substantial, economically justified processing or working

- in an undertaking equipped for that purpose

- resulting in the manufacture of a new product or representing an important stage of manufacture

A processing or working is not considered to be substantial, economically justified if it is a minimal operation. Article 34 of the UCC-DA lists the minimal operations:

- Operation to ensure preservation during transport or storage

- Simple operations consisting of removal of dust, sifting or screening, sorting, classifying, matching, washing, cutting up.

- (changes of) packing, assembly, other simple packaging operations

- Putting up goods in sets or ensembles

- Affixing marks, labels, etc.

- Assembly of parts into complete product

- Disassembly

- A combination of the above

If goods are listed in Annex 22-01 to the UCC-DA then the last substantial, economically justified working or processing is the one mentioned in this Annex. The country or territory where this working or processing has taken place is where these goods originate. Currently this Annex 22-01 doesn't apply to mineral oils, (bio)ethanol and biodiesel.

A refinery process ticks all 3 boxes. It is a substantial, economically justified processing or working. It takes place in an undertaking equipped for that purpose and it results in the manufacture of a new product or it represents an important stage of manufacture.

A blend process is less clear in terms of non-preferential origin. Not every blend process will make the origin change. If you're blending different fuel oil grades in order to change viscosity, this might not be sufficient to result in a different origin. if you're blending biodiesel with diesel into B7, arguably this changes the origin based on rule 2.

Residual rule

If the activity does not result in a change of origin following rule 1 or rule 2 while the activity entails more than a minimal operation then the residual rule applies. This rule is usually referred to as majority rule although calling it the major portion rule would be more accurate.

Under this residual rule the country of origin is the country where the major portion of the components used in the activity originate. The major portion is determined on the basis of:

- The weight of the used components; HS chapters 1-29 and 31-40

- The value of the used components; HS chapters 30 and 41-97

Our products generally fall under chapter 27 and sometimes chapter 22 (ethanol), 29 (butane) or 38 (FAME)

Proof of origin

The non-preferential origin is demonstrated via a Certificate Of Origin (COO). Each EU Member State decides on the competent authority for issuing COOs. In most EU Member States the Chamber of Commerce or a similar body is competent to issue a COO.

A COO is only issued when evidence of compliance with the rules of origin is provided

- Details of the blend

- Details of the operation (proof it is economically justified etc.)

- Evidence of the origin of the blend components in case the majority rule applies

- Evidence of the weight of the blend components in case the majority rule applies

Some examples

Example 1

Example 2

We?re blending gasoline for export to West Africa in Amsterdam. All components have a different CN Code. The blend consists of the following components:

- Component A / Dutch origin / Value of USD 500,000 / Weight 4kt

- Component B / Norwegian origin / Value of USD 600,000 / weight 8kt

- Component C / UK origin / Value of USD 700,000 / weight 6kt

- Component D / Norwegian origin / Value of USD 200,000 / weight 1kt

-

We have two options to determine the origin of this blend

- This is an economically justified processing or working. The blend has Dutch origin as that?s the country where this activity takes place.

- This is not an economically justified working or processing. The ?majority rule? applies. Based on the weight, the major portion of the components used have Norwegian origin. The full blend is considered to be of Norwegian origin.

Preferential origin

Legal basis

Preferential origin is primarily based on Free Trade Agreements (FTA). FTAs are reciprocal. Based on the FTA between the EU and Morocco, products of EU preferential origin can be imported at preferential duty rates into Morocco and products of Moroccan preferential origin can be imported at preferential duty rates into the EU.

In order to understand the rules of origin we need access to each individual FTA. Every FTA has a protocol that is dedicated to these rules of origin. The European Commission maintains a list with links to the various FTAs the EU has signed up to. This list can be accessed here: EU FTA List

In addition to the reciprocal FTAs, the EU also grants preferential origin benefits on a unilateral basis. These legal provisions can be found here:

Articles 64 - 68 UCC (Union Customs Code)

Articles 37 - 70 UCC-DA (Union Customs Code Delegated Act)

Articles 60 - 126 UCC-IA (Union Customs Code Implementing Act)

Preferential rules of origin

Rule 1 - wholly obtained

Goods are of non-preferential origin in the single country or territory where these goods are wholly obtained. This reference to country or territory includes territorial waters. It also includes the seabed or subsoil beneath the seabed to which a country has exclusive exploitation rights.

Some examples:

- Crude produced in the USA is of USA origin

- Crude produced outside The UK, from seabed or subsoil beneath the seabed to which The UK has exclusive exploitation rights, is of UK origin

- Diesel produced in Norway out of crude of Norwegian origin is of Norwegian origin under this rule as the product is wholly obtained in a single country

Rule 2 - non originating materials having undergone sufficient working or processing

This is a very specific rule of which the details will differ per FTA. Each FTA contains an annex that contains detailed rules per CN Code on the requirements that need to be fulfilled in order to generate a product that is of preferential origin. In order to determine preferential origin, the applicable FTA needs to be consulted, but as a general rule the following elements can play a role in determining preferential origin:

- Refining processes generally are sufficient to make the product qualify as having preferential origin

- Blending processes generally are not sufficient to make the product qualify as having preferential origin

- A change of tariff heading (first 4 digits of the CN Code) is generally sufficient to make the product qualify as having preferential origin

- There can be value restrictions as to the maximum amount of non-preferential materials that can be used in a production process

- There can be quantity restrictions as to the maximum amount of non-preferential materials that can be used in a production process

Each FTA also contains a detailed list of activities that are deemed to be an insufficient working or processing. Those activities will never result in a product that has preferential origin.

There is no residual origin rule in relation to preferential origin. if a product meets all requirements, it is of preferential origin. If it doesn't meet all requirements the product is not of preferential origin.

Direct Transport

In order to maintain the preferential origin, each FTA requires that the product is directly transported from the country of origin to the country of importation. However, products may be transported through other territories provided that they remain

under the surveillance of the customs authorities in the country of transit or warehousing and do not undergo operations other than unloading, reloading or any operation designed to preserve them in good condition. The importer claiming preferential origin at import has to provide evidence to customs that the direct transport rule has been met. Any evidence can provided to demonstrate compliance with the direct transport requirement. Examples of this are:

- a single transport document covering the passage from the exporting country through the country of transit

- a certificate issued by the customs authorities of the country of transit:

- giving an exact description of the products;

- stating the dates of unloading and reloading of the products

- where applicable, the names of the ships, or the other means of transport used;

- certifying the conditions under which the products remained in the transit country; or

- any other substantiating document.

In some FTAs this requirement is referred to as the non-alteration clause. This clause functions the same way as the direct transport clause.

In most FTAs the burden to proof compliance with the direct transport rule is on the importer, but exceptionally an FTA deem this rule to be met and require the customs authorities to provide evidence that this direct transport rule has not been met.

Proof of preferential origin

The exporter of the goods arranges for the proof of preferential origin. The way this is done depends on the applicable FTA and simplifications applied for by the exporter.

The standard proof of preferential origin is the EUR.1 certificate. This certificate is issued by customs of the country of export upon request of the exporter. The EUR.1 certificate is a paper certificate of which the original hard copy needs to go to the importer in order to enable the importer to claim the reduced preferential import duty. The mandatory template of the EUR.1 is included in the annex of each FTA that still recognizes the EUR.1 as proof of origin. Customs will only issue the EUR.1 if there is evidence that the product meets the preferential origin criteria. This evidence is provided via a supplier's declaration. Via this supplier's declaration customs can follow the supply chain back to the place where the product obtained its preferential origin. In our case this is usually the refinery that produced the fuel.

Exporters who are authorized by customs as approved exporter can replace the EUR.1 certificate by a so called invoice declaration. This invoice declaration is a statement about the preferential origin that the approved exporter can print on the invoice or on any other commercial document. The wording of this statement is provided for in the annex of each FTA in each official language. It is not allowed to deviate from this wording. An origin statement that deviates from the version prescribed in the FTA does not qualify as a valid preferential origin statement.

The approved exporter permit contains a list of locations from where we can export preferential product by issuing a preferential statement of origin on a commercial document. If we want to use this permit from other locations we need to notify customs in advance and add this location to our permit. This doesn't take a lot of time, but needs to happen.

The approved exporter permit is based on a description of our internal procedures and our internal risk management processes, called AO-IB. Customs only grants the approved exporter permit if they are confident that we have implemented strong processes to avoid that we issue a preferential statement on origin for products that do not qualify as having preferential origin. Customs will periodically perform an audit to ensure that we still apply the agreed procedures as described in our AO-IB.

In short, the process to self issue a preferential statement on origin is as follows:

- Request

- Include following details:

- The document on which the preferential statement of origin has to be printed

- The deal number

- The country of destination. This information is necessary to identify the applicable FTA

- Evidence that the goods qualify as having preferential origin. Usually this is a supplier's declaration issued by our supplier.

- Based on this information the request will be processed. The document holding the preferential statement on origin will be send by e-mail to the requestor for further distribution to customer